The first hospital bill arrived three weeks after you brought the baby home. Then another one came from a doctor you don’t remember meeting. Then a third from a lab. None of the numbers match each other, and none of them match what your insurance company already sent you. Welcome to the part of healthcare nobody warned you about.

We’ve talked to a lot of parents about this moment. The bills are confusing on purpose — different entities bill separately, the codes are opaque, and the “patient responsibility” line is often wrong on the first pass. The good news: most of these bills can be reduced, corrected, or in some cases eliminated, if you know what to look at and in what order. Here’s how to work through it without losing your mind.

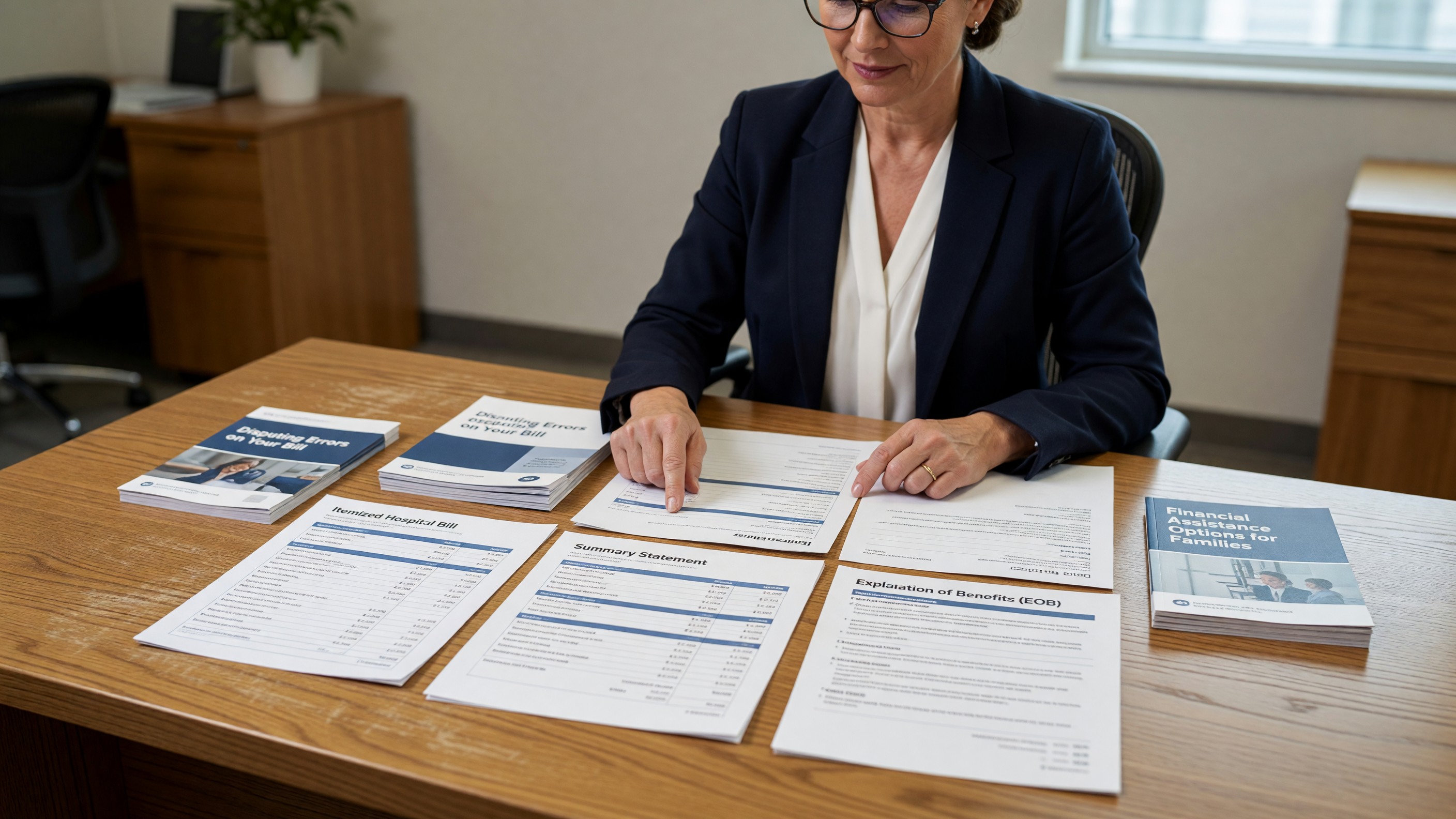

The three documents you actually need

Before you can do anything else, gather these three things. If you only have one of them, that’s the first problem to fix.

1. The itemized bill from the hospital. This is the detailed, line-by-line list of every charge — every dose of medication, every room day, every blood draw, every imaging study. Hospitals don’t always send this automatically. What they send is often a “summary bill” with one or two big numbers and a balance due. You have a right to request the itemized version, and you should — that’s where the errors live.

2. The Explanation of Benefits (EOB) from your insurance. This is not a bill. It’s a statement from your insurance company explaining what the hospital charged, what your insurer “allowed” (the negotiated rate), what they paid, and what they say you owe. Your insurer’s portal will have it. The U.S. Department of Health and Human Services has a plain-language explanation of EOBs on healthcare.gov.

3. The summary bill or final statement. This is what the hospital is asking you to pay. The number on this should match the “patient responsibility” line on the EOB. Often it doesn’t, which is the second problem to fix.

When all three documents are in front of you, lay them out side by side. The itemized bill should explain what you were charged for. The EOB should explain what your insurance did with those charges. The summary bill should reflect what’s left for you. If those three don’t line up, something is wrong, and that something is usually fixable.

Terms that mean specific things

A handful of words come up over and over in hospital billing. They’re not interchangeable, and the difference between them is sometimes hundreds or thousands of dollars.

- Billed charge (or gross charge). What the hospital initially charges. This number is almost meaningless — it’s the list price nobody really pays.

- Allowed amount. The negotiated rate between the hospital and your insurance company. This is the number that actually matters. Anything above this, in-network, is supposed to be written off.

- In-network rate. The allowed amount when the provider is contracted with your insurer.

- Out-of-network rate. What gets charged when the provider doesn’t have a contract with your insurer. Historically this is where the worst surprise bills came from.

- Patient responsibility. Your share — deductible, copay, coinsurance, plus any non-covered charges. This is what should appear on your final bill.

- Balance billing. When a provider tries to bill you for the difference between their billed charge and what insurance allowed. In many situations this is now illegal (more on that below).

- EOB. Explanation of Benefits. The insurance statement, not a bill.

- Coinsurance. A percentage of the allowed amount you pay after meeting your deductible — for example, 20% of an allowed $1,000 charge would be $200.

If you only remember one thing from this section: the allowed amount is the real number. When you’re negotiating or disputing, that’s the line to focus on.

The No Surprises Act — protections you actually have

Since January 2022, federal law has protected most patients from many of the worst out-of-network surprise bills. The Centers for Medicare & Medicaid Services maintains an official overview of the No Surprises Act that covers what’s protected and what isn’t.

Here’s the short version of what the law does for families with a NICU or inpatient stay:

- Emergency services at any facility are billed as if in-network, even if the hospital or treating physician is out-of-network.

- Non-emergency services at an in-network facility by out-of-network providers (the anesthesiologist, the radiologist, the pathologist — providers patients almost never get to choose) are billed at in-network rates.

- Air ambulance services are subject to the same protections.

If you find a surprise out-of-network charge that should have been protected, you can file a complaint with the federal government through the No Surprises Help Desk (1-800-985-3059). Don’t pay the disputed amount while it’s being reviewed.

The law also requires uninsured and self-pay patients to receive a “good faith estimate” before scheduled care. If the actual bill comes in more than $400 over that estimate, you can dispute it through the federal patient-provider dispute resolution process.

Common errors to scan for first

Before you call anyone, sit down with the itemized bill and look for these specific patterns. They’re the most common, and the easiest to get reversed.

Duplicate charges. The same medication, lab, or procedure listed twice on the same date with no clear reason. Maternity and NICU bills are especially error-prone here because so many small charges accumulate during a long stay.

Charges for items that should be bundled. Operating room time billed alongside individual gauze, gloves, sutures, and supplies that are typically included in the OR charge. The American Hospital Association and Medicare both publish bundling rules; ask the billing department for a written explanation if you see a charge that looks like it should be part of something else.

Never-events. Procedures or complications that should never have happened and which Medicare and many insurers refuse to pay for at all. If a hospital billed for a wrong-site surgery, a serious medication error with patient harm, or certain hospital-acquired infections, that charge is often not the family’s responsibility.

Observation vs. admission. This one trips up families constantly. If your child was “in observation” rather than admitted as an inpatient, the billing rules — and what insurance pays — change significantly. Check the bill against your hospital records. If you remember the doctor saying “we’re admitting them” but the bill is coded as observation only, ask why.

Wrong dates. A charge listed on a date your child wasn’t in that unit, or wasn’t in the hospital at all.

Wrong patient identifier. Hospitals sometimes mix up records across patients with similar names or shared family records. Rare but it happens.

When you find something, write down the line item, the date, the charge, and what you think is wrong. That list becomes your dispute document.

How to actually request an itemized bill

If you only got the summary, request the itemized version in writing. Email is fine; many hospital patient portals have a “request itemized statement” option built in. If you have to do it by phone, follow up the call with an email summarizing what you asked for and when.

Keep the language simple: “I am requesting a fully itemized statement of all charges for [patient name], account number [X], for the dates of service [X to Y]. Please include CPT, HCPCS, and revenue codes for each line.”

The CPT and revenue codes matter because they let you (or anyone helping you) verify what the charge is actually for. Without codes, “supply — misc” could be anything.

Federal regulations under the Hospital Price Transparency Rule also require hospitals to publish their standard charges and negotiated rates publicly — so for many big-ticket items, you can cross-check what the hospital is billing against what they’ve publicly stated they charge insurers.

Disputing charges — the actual process

The “call the billing office” advice is real but incomplete. Here’s the sequence that actually tends to work.

Step 1: Call your insurance company first, not the hospital. Ask them to walk you through the EOB. Get the name of the person you spoke with and a reference number for the call. Often the insurer can identify the error before the hospital even sees it.

Step 2: File a formal claim review or appeal with your insurer if the EOB is wrong. Every insurer has an internal appeals process — they’re required to. The denial or EOB notice itself tells you the deadline. Don’t miss it.

Step 3: Send a written dispute to the hospital billing department. Reference the specific line items, the dates, and what’s wrong. Ask them to put your account on hold during the review so it doesn’t go to collections. They are usually willing to do this; if not, escalate to the patient advocate.

Step 4: Ask for a patient advocate or financial counselor. Most hospitals have one. They are not the same as the billing office, and they often have more authority to write down charges or set up assistance.

Step 5: If your insurer’s internal appeal fails, request an external review. Under the Affordable Care Act, most plans must allow an independent external review for denied claims. The Department of Labor’s guide to ERISA appeals covers this for employer-sponsored plans.

Step 6: If the hospital refuses to budge and you still believe the bill is wrong, you can file a complaint with your state’s attorney general or department of insurance. Both have consumer protection arms. State complaints get hospital billing departments to call back faster than almost anything else.

Throughout all of this, keep a single folder (paper or digital) with every letter, email, call note, and document. If a bill goes to collections during a dispute, that documentation is what protects you.

Financial assistance — the rule most families don’t know about

If your hospital is a nonprofit — and roughly half of U.S. hospitals are — federal law requires it to offer a financial assistance policy under Section 501(r) of the tax code. The IRS publishes requirements for charitable hospitals under section 501(r), which include having a written financial assistance policy, publicizing it, and limiting what they can charge people who qualify for assistance.

What this means in practice:

- The hospital must have a financial assistance policy (FAP) and make it easy to find.

- Patients who qualify cannot be charged more than the “amounts generally billed” to insured patients.

- Hospitals cannot pursue aggressive collection actions (lawsuits, wage garnishment, credit reporting) until they’ve made reasonable efforts to determine whether you qualify for assistance.

Even for-profit hospitals often have charity care or financial assistance programs, though they’re not required by federal law to offer them. State laws in many states require them anyway.

Ask for the financial assistance application before you pay anything. If you’ve already paid and you would have qualified, you may be able to get a refund — many policies look back 240 days or longer.

Once you’ve worked through your own family’s bill, the facility-billing side of all this — how hospitals structure their charges, what the rules are for nonprofit status, and how compliance gets enforced — is covered on our sister site, Healthcare Facility Guide. It’s a useful resource if you want to understand what the hospital is dealing with on its side of the conversation.

What to do this week

If you’re staring at a bill right now and not sure where to start:

- Request the itemized statement (in writing).

- Pull the matching EOB(s) from your insurance portal.

- Compare line by line and circle anything that doesn’t match.

- Call your insurer to walk through any mismatch before calling the hospital.

- Ask the hospital about their financial assistance policy in the same conversation you raise disputes — there is no penalty for asking.

- Keep every document in one folder.

You may also find it helpful to read our guide to finding a hospital social worker — social workers handle billing escalations all day long and can often shortcut a process that would take you weeks.

Frequently asked questions

How long do I have to pay a hospital bill before it goes to collections?

It varies by hospital. Most have a 90- to 120-day window before sending an account to collections, but federal rules for nonprofit hospitals require them to make reasonable efforts to determine your eligibility for financial assistance first — typically 120 days from the first post-discharge billing statement and at least 240 days before extraordinary collection actions. Always ask for the account to be placed on hold while a dispute or application is in process.

Is the No Surprises Act retroactive?

No. The protections apply to services on or after January 1, 2022. If you have a bill from before that date and the surprise out-of-network charge was the issue, your state may have its own balance-billing protections — many states do.

Can I negotiate the price even if there are no errors?

Often, yes. If you’re uninsured or paying cash, hospitals will frequently accept 30–50% of the gross billed amount. If you’re insured but have a large deductible, you can ask about prompt-pay discounts. Nothing about asking puts you in a worse position.

Should I put a hospital bill on a credit card to pay it off?

Generally no. Hospitals are usually willing to put you on a 0% payment plan; credit cards are not. Once a charge is on a card, you also lose some of the rights you have while the bill is still with the hospital — including the protection against extraordinary collection actions for nonprofit hospitals.

What if my child was on Medicaid or CHIP — do I still need to worry about a bill?

You shouldn’t be receiving balance bills for covered services if Medicaid was active during the stay. If you do, that’s a billing error and should be disputed immediately. Our guide on Medicaid for children, state by state covers what’s supposed to be covered and what to do if a provider tries to bill you anyway.

The bill says “courtesy charge” — what is that?

Usually it’s a discount the hospital is applying. Sometimes it’s used to label charges they think they’re being generous about. Ask for the line to be explained in writing.