Medicaid for kids is one of the few parts of the U.S. healthcare system designed to actually work for low- and middle-income families. The catch is that every state runs its own version of the program, and the rules — income limits, paperwork, even what the program is called — change at the state line. We’ve talked to parents who didn’t realize their child qualified for years, and others who lost coverage during a renewal cycle they didn’t know was happening. This guide is a starting point for figuring out where your family stands.

Two things to know upfront. First, we are not going to publish specific dollar thresholds for state income limits in this guide. Those numbers change every year, and the wrong figure on the wrong day can cost a family coverage. Instead, we’ll show you exactly where to look up the current limit for your state. Second, eligibility for children is generally much more generous than eligibility for adults — children commonly qualify in households where neither parent does.

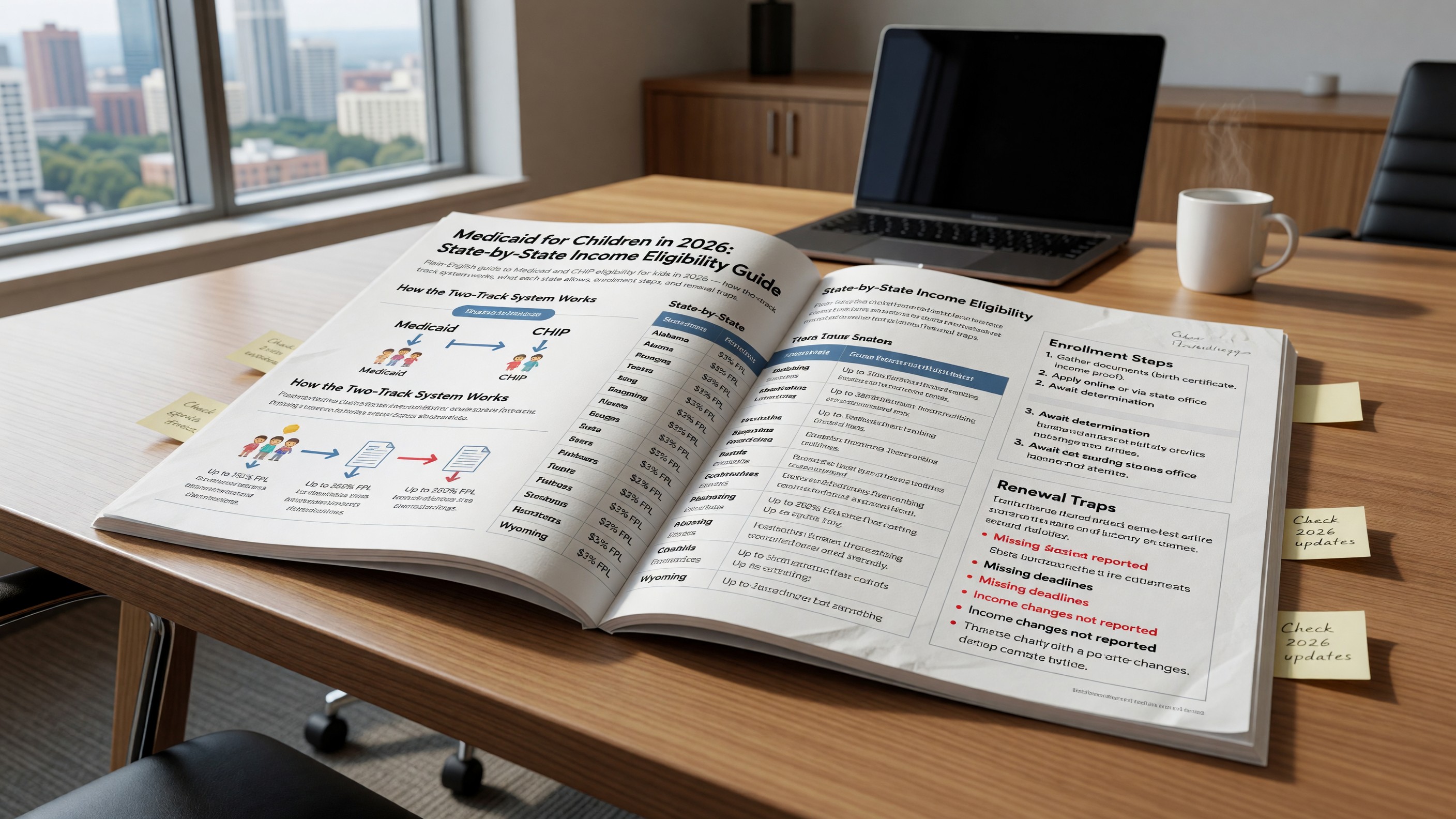

The two-track system: Medicaid and CHIP

For kids under 19, two programs work together: Medicaid and the Children’s Health Insurance Program (CHIP). They share enrollment systems in most states, and from a parent’s perspective they often look like the same program — but they’re funded and structured differently, and the rules diverge in ways that matter.

Medicaid is a joint federal-state program that covers low-income individuals and families. The federal government sets minimum standards and matches state spending; states administer it and can choose to be more generous than the federal floor. The official Medicaid program page at medicaid.gov is the federal hub.

CHIP is a sibling program designed for kids whose family income is too high for Medicaid but too low to comfortably afford private coverage. It typically covers the same essential pediatric services. Some states run CHIP as a separate program; others fold it into Medicaid. CHIP’s overview page explains the federal framework.

For families, what this means is straightforward: in nearly every state, children have a path to coverage at much higher income levels than adults do. If you’ve been told you don’t qualify for adult Medicaid in your state, do not assume the same is true for your kids. The kid-specific limits are almost always higher — often much higher.

Federal floor versus state expansion

Federal law sets a minimum that every state must meet for children’s Medicaid eligibility. States are then free to expand from there, and most have.

The federal floor for children’s Medicaid coverage is based on the Federal Poverty Level (FPL), which the U.S. Department of Health and Human Services updates annually. The current poverty guidelines are published by HHS Poverty Guidelines and updated each January.

In broad terms, federal law requires states to cover:

- Infants (under age 1) at family incomes at or above a defined percentage of FPL.

- Children ages 1 to 5 at a defined (typically lower) percentage of FPL.

- Children ages 6 to 18 at a defined percentage of FPL.

Most states cover children well above these federal floors. The combined Medicaid + CHIP eligibility for kids commonly reaches somewhere in the 200%–300% of FPL range, and a handful of states go meaningfully higher. The Kaiser Family Foundation’s state Medicaid income eligibility limits for children is the cleanest place to compare states side by side.

The takeaway: even if your household is well above what you’d call “poverty,” your kids may still qualify. Don’t self-disqualify based on a number you remember from years ago.

How to find your state’s exact eligibility

The single best move is going directly to your state’s Medicaid agency. Federal resources help you compare; state resources tell you what you actually qualify for.

Step 1 — Find your state’s Medicaid page. Medicaid.gov maintains a state Medicaid and CHIP profiles directory that links to every state agency.

Step 2 — Use the federal marketplace as a backup. HealthCare.gov can screen your family for Medicaid and CHIP eligibility when you apply for a marketplace plan. If your kids qualify, it’ll redirect that part of the application to your state. This is useful when you’re not sure where the line is and want a quick sanity check.

Step 3 — Cross-check with KFF. The Kaiser Family Foundation publishes a 50-state comparison of children’s Medicaid and CHIP income limits, updated as states change their rules. KFF expresses limits as a percentage of FPL, which is the format used in federal rule-making — so it stays consistent across years even when the dollar figures change.

Step 4 — Call the state agency if anything is unclear. State Medicaid offices have parent navigators in most states. They are not gatekeepers — their job is to enroll eligible families.

What you need to enroll

When you apply, you’ll typically need:

- Proof of identity for parents/guardians (driver’s license, state ID, passport).

- Proof of citizenship or qualified immigration status for the child being enrolled (birth certificate, naturalization certificate, or relevant immigration document).

- Proof of income (recent pay stubs, last year’s tax return, unemployment statements, self-employment records). Most states use Modified Adjusted Gross Income (MAGI) rules for kids, which match what’s on your federal tax return.

- Proof of residency in your state (utility bill, lease, school enrollment record).

- Social Security numbers for each applicant (children without SSNs can still be enrolled in many cases — ask).

Timeframes you should know:

- Most states process applications within 45 days.

- Newborns of a parent already on Medicaid at birth are generally automatically eligible for at least their first year.

- Retroactive eligibility is available in many states — meaning if your child was hospitalized before you applied, the coverage can sometimes be made effective for up to three months before the application date. This is one of the most important and least-discussed features of the program. Ask about it explicitly.

- Presumptive eligibility exists in many states, allowing certain providers (hospitals, qualified clinics) to grant temporary coverage on the spot while a full application is processed.

If a child is born during a hospital stay and you don’t have coverage in place, ask the hospital social worker about applying through the hospital. Our guide to finding a hospital social worker walks through that process.

State-by-state notes — generosity tiers

States vary in how generous their children’s coverage is. Without quoting specific 2026 dollar figures (which would be out of date almost immediately), here’s how to think about your state.

Highest-generosity states — typically include New York, Massachusetts, California, New Jersey, Vermont, Connecticut, Washington, and a handful of others. These states have expanded both adult Medicaid under the Affordable Care Act and have raised children’s Medicaid/CHIP limits well above the federal floor. Many cover kids up to 300% of FPL or higher.

Mid-generosity states — most states fall here. They’ve expanded children’s coverage above the federal floor, usually somewhere in the 200%–300% of FPL range, often with a separate CHIP program covering the higher end of that range.

Lower-generosity states — historically include some states that have not expanded Medicaid for adults, like Texas, Florida, Mississippi, Alabama, Georgia, and Tennessee. Even these states, however, cover children well above adult thresholds, often around 200% of FPL or higher for kids specifically. Children’s eligibility in non-expansion states is still often quite generous — do not assume your kids don’t qualify because the state hasn’t expanded Medicaid for adults.

For comparison data across all 50 states, the KFF state health facts on Medicaid and CHIP is regularly updated and is the resource we use most often.

A handful of states (notably Ohio, Pennsylvania, Michigan, and others) sit somewhere between mid- and high-generosity. Limits can shift after a state legislative session or a federal rule change, so always verify the current number directly with your state.

CHIP — for kids above the Medicaid line

CHIP is purpose-built for the income range where families earn too much for Medicaid but not enough to comfortably buy private coverage. Premium and copay structures vary, but they’re modest — designed to be affordable.

What’s covered under CHIP, per federal requirements, includes:

- Routine well-child visits

- Immunizations

- Doctor visits and prescriptions

- Dental and vision care

- Hospital and emergency care

- Lab and X-ray services

CHIP coverage is, in most states, comparable to a high-quality private plan with very low out-of-pocket costs. The CHIP eligibility overview at medicaid.gov explains what every state’s program has to include at minimum.

If your kids are denied Medicaid because income is slightly too high, the application is typically forwarded automatically to CHIP. Don’t take a Medicaid denial as the end of the road.

What happens at age transitions

Two transitions trip up families regularly.

Newborn → child Medicaid. A baby born to a Medicaid-enrolled parent is generally deemed eligible for the first year automatically — no separate application needed during that first year. But you do need to make sure the baby is added to Medicaid promptly so claims are paid. Ask the hospital before discharge or call the state agency in the first few weeks.

Medicaid → CHIP at higher ages or income changes. As kids get older, some states phase down Medicaid eligibility and pick up coverage through CHIP. The transition is supposed to be seamless. In practice, families sometimes get a notice they don’t understand and assume coverage is ending. Read every Medicaid letter; if it says your child is being moved to CHIP, that’s still coverage — just a different door.

The most common breakdown point is when a family’s income increases mid-year and the state re-evaluates eligibility. That’s where coverage gaps happen, usually because a parent didn’t respond to a renewal form. Which brings us to renewals.

Renewal traps and the “unwinding”

During the COVID-19 public health emergency, states were required to keep people enrolled in Medicaid continuously — meaning no annual renewals. That ended in 2023, and the resulting “unwinding” caused millions of children to lose coverage, many of them for paperwork reasons rather than because they were no longer eligible.

KFF has been tracking the impact of unwinding closely. Their Medicaid enrollment and unwinding tracker is the best place to see what’s happened state by state.

The lessons from unwinding, even now that the initial surge is over:

- Annual renewal is back. Most kids must be re-verified for eligibility every 12 months. Some states have moved to 12 months of continuous eligibility for kids — once enrolled, kids stay covered for a full year regardless of mid-year income changes.

- Renewal notices often go to outdated addresses. If you’ve moved, update your address with the state agency immediately. This is the single most common reason kids lose coverage.

- Some renewals are “ex parte” — meaning the state can re-verify using existing data and re-enroll the child automatically without you doing anything. If you’re not sure whether yours was renewed, log into your state portal and check.

- There’s typically a 90-day reconsideration window after a Medicaid termination during which the state will re-enroll a child if they’re still eligible, without making you start a new application. If your child was just dropped, call immediately.

If a child loses Medicaid for paperwork reasons and you’re inside the reconsideration window, that’s the first call to make.

For families looking at the broader picture of facility-side billing rules and how hospitals interact with Medicaid programs, our sister site Healthcare Facility Guide covers that operational side in detail.

What to do this week

If you think your child might qualify or you’re not sure:

- Pull up the Medicaid state overviews page and find your state.

- Have last year’s tax return and a recent pay stub ready.

- Apply through your state’s portal or through HealthCare.gov.

- If you’ve had a denial in the past, re-apply — limits and household composition change.

- If your child was recently dropped, ask about the 90-day reconsideration window.

For a deeper look at what to do once a child is admitted to a hospital and you’re navigating the system in real time, see our NICU survival guide and how to read your hospital bill after a NICU or inpatient stay.

Frequently asked questions

Can my child qualify for Medicaid even if I don’t?

Yes — and this is one of the most important things parents miss. In every state, the income limits for children’s Medicaid and CHIP are higher than the limits for adult Medicaid. It is very common for kids to qualify in families where neither parent does.

What if we’re between jobs or our income changed mid-year?

Most states use current monthly income for Medicaid eligibility, not last year’s tax return. If your income dropped recently, apply right away — don’t wait for the next tax year. Some states also have continuous eligibility for kids, which means once a child is enrolled they stay enrolled for a full 12 months regardless of mid-year income changes.

Does Medicaid cover dental and vision for kids?

Yes. Federal law requires Medicaid to cover dental and vision services for children under the Early and Periodic Screening, Diagnostic, and Treatment (EPSDT) benefit. CHIP coverage of dental and vision is also required.

My child has special needs — does that affect eligibility?

It can help. Many states have additional Medicaid pathways for children with disabilities or specific medical conditions — including the Katie Beckett option in some states, which allows children with serious medical needs to qualify based on the child’s own income and assets rather than the family’s. Ask your state Medicaid office about disability-based eligibility specifically.

Can a child be on both Medicaid and private insurance?

Yes. This is sometimes called “secondary coverage” or “wrap-around coverage.” Medicaid pays after the private insurance pays. Many families with high-deductible private plans find this combination valuable for kids with significant medical needs.

What if I’m undocumented but my child is a U.S. citizen?

Your child’s eligibility is based on the child’s status, not yours. U.S. citizen children of undocumented parents are fully eligible for Medicaid and CHIP if they meet the income criteria. State Medicaid offices are not federal immigration enforcement; the information you provide for your child’s application is used for eligibility determination only.

How long does it take to get approved?

Most states process applications within 45 days. Newborn additions to an existing Medicaid case can be much faster, sometimes same-day. Presumptive eligibility programs (where available) can grant coverage immediately while the formal application is reviewed.